Karen Purze is an author based in Chicago, IL. She writes about end-of-life planning and family caregiving at lifeinmotionguide.com.

A primer to help you consider your needs and understand your options

If you’ll be turning 65 soon, it’s time to start thinking about Medicare coverage. Before you enroll, though, take the time to learn about your choices.

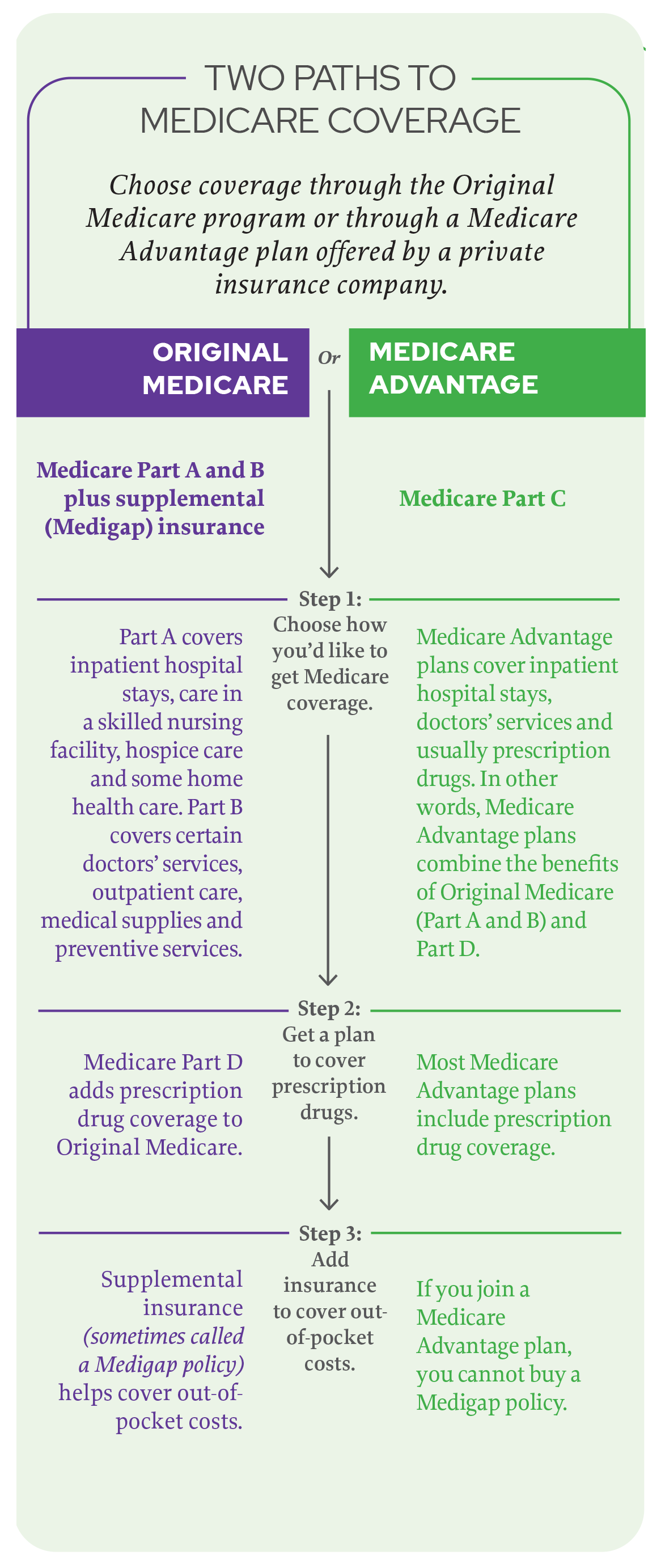

Your first step is to understand your options. At the simplest level, you have a choice of signing up for Original Medicare or joining a Medicare Advantage plan.

Individuals who choose Original Medicare — which is Medicare Part A (hospital insurance) and Part B (medical insurance) — typically also buy supplemental coverage (sometimes called a Medigap policy) and prescription drug coverage (Part D) to control their out-of-pocket costs. The supplemental plans help cover co-pays and co-insurance fees and help protect you from high costs if you go to the doctor frequently or experience an unexpected health event.

Medicare Advantage plans (sometimes called Part C) are offered by companies that contract with the federal government to offer Medicare benefits, usually through a defined network of providers (similar to an HMO or PPO).

Medicare Advantage plans typically cover the full range of benefits offered by Medicare Part A, Part B and Part D (prescription drugs) — and sometimes much more. Medicare Advantage plans can be more affordable than Original Medicare if you are relatively healthy and your doctors are part of the plan’s network, or if you’re open to changing doctors. Be aware that some Medicare Advantage plans may not cover care outside their service area.

Picking a plan

Determining which path is best for you depends on factors such as your health, what type of plan your doctors accept, how much you travel outside your plan’s service area (whether you travel internationally or spend part of the year away from your primary residence) and whether you’re employed.

“The good thing is you have a choice,” says Peter Miska, president of Phoenix Home Care, LLC, a Medicare-certified home health agency serving the Chicagoland area. “The hard thing is you have to make the right choice.”

Some Medicare Advantage providers may expand certain benefits while others may choose to focus on core benefits and lowering out-of-pocket expense, says Matthew Post, senior vice president of sales and marketing at Clear Spring Health, which provides Medicare Advantage plans in Illinois and several other states.

“In recent years, the Centers for Medicare & Medicaid Services (CMS) has loosened certain regulations, allowing payers to offer new benefits and be more creative with supplemental benefits,” he says. Some providers are launching new plans that include assistance with food insecurity, personal care, transportation, nutrition education and other wellness offerings.

Because of the COVID-19 pandemic, Medicare has broadened access to telehealth services for Original Medicare. Medicare Advantage plans have historically offered more telemedicine benefits. “The recent pandemic has pushed telemedicine to the forefront of what was an already expanding benefit,” Post says.

Consider your drug needs

Before you decide whether to choose Original Medicare (with separate Part D prescription drug and supplemental Medigap insurance plans) or a Medicare Advantage plan that includes drug coverage, take a step back and consider your needs.

Use the tools on medicare.gov to compare plans and determine whether a plan’s provider network includes your preferred physicians.

Next, compare costs for your prescription drugs using the tools on the medicare.gov website. There are many different Part D plans, and each has its own formulary — the list of drugs it covers. Drug prices and coverage can vary widely. It pays to do your research, especially if you have chronic or disabling conditions that require multiple prescriptions to manage.

“I see people consistently overspend for prescriptions because they are not in a suitable drug plan for their specific medications,” says Robin Dawson, an independent insurance broker at Medicare Solutions Network, located in Lisle. “These plans are not all the same, and every year the plans may change premiums, their covered formulary or preferred pharmacy partners.” For example, a drug that was on the plan’s formulary last year may not be on it this year, causing it to be significantly more expensive.

Examine employee options

If you are employed (or covered by a spouse’s employer), talk with the benefits administrator to determine how your current insurance may or may not be combined with Medicare.

If you’re over 65 and have group health plan coverage based on your or your spouse’s current employment, you may be able to defer enrollment in full Medicare coverage without paying the penalty that is charged if you enroll after your initial enrollment period ends.

In one common scenario, you would enroll in Medicare Part A at no cost and maintain coverage through your employer for everything else, deferring enrollment in Part B. Alternatively, you could choose to buy an individual Medicare Advantage plan when you become eligible.

“People should know they have options,” says Richard Kozlowski, principal of LifeSmart Senior Services, an Elgin-based insurance agency focused on the needs of seniors.

“Sometimes we find an individual Medicare Advantage plan saves an employee money [over their employer coverage]. There are also cases where it’s in a person’s best interest to stay on the [employer’s] group plan,” Kozlowski says.

Sign up on time

Once you’ve determined which plan best meets your needs, you may be ready to sign up — unless you’re automatically enrolled.

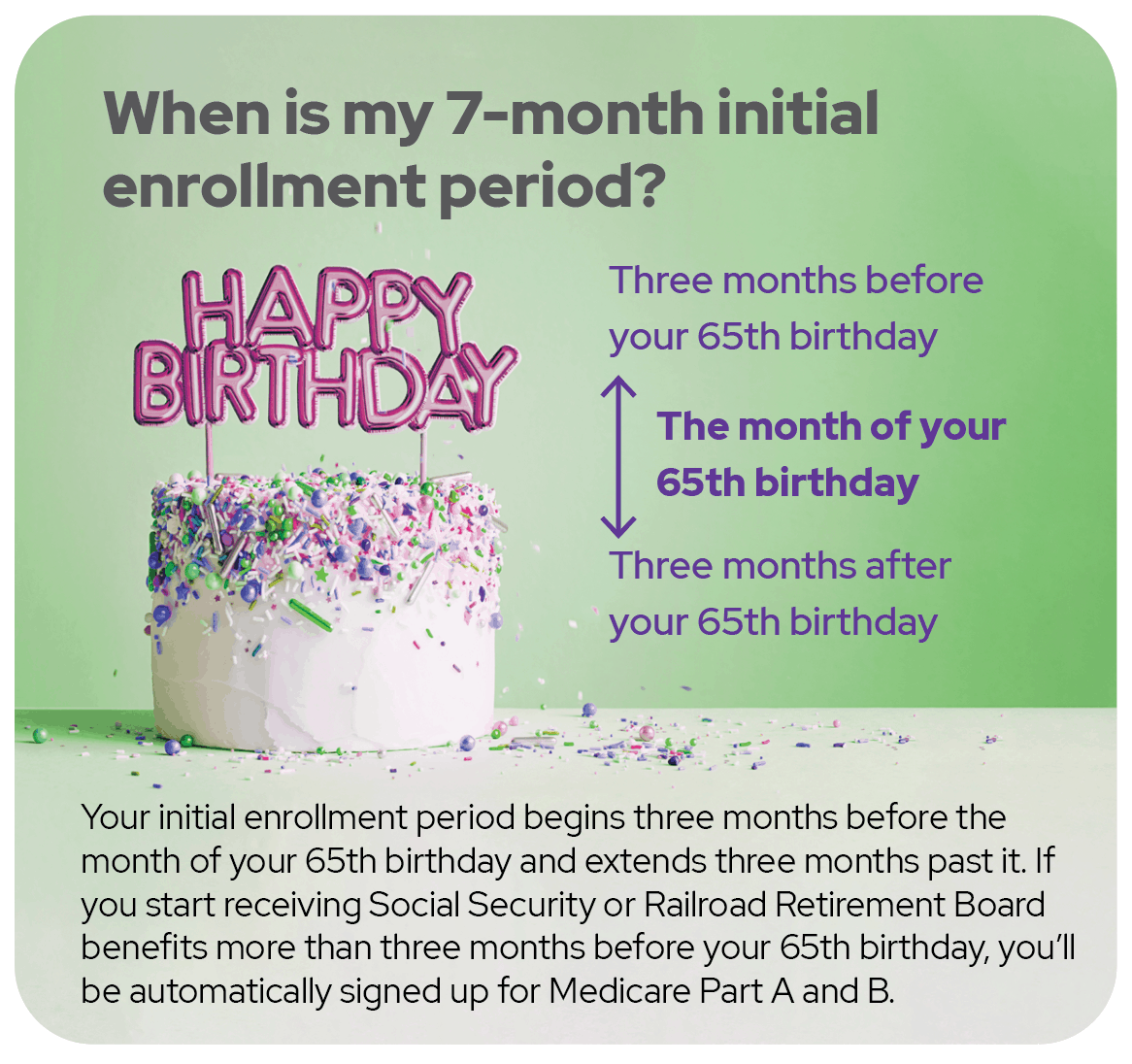

If you start receiving Social Security or Railroad Retirement Board benefits more than three months before your 65th birthday, you’ll be automatically signed up for Medicare Part A and Medicare Part B.

Otherwise, you’ll need to enroll during the initial enrollment period, which starts three months before your 65th birthday month and extends three months past it. Sign up for Medicare online at socialsecurity.gov or by calling the Social Security Administration at 800-772-1213.

There is a penalty if you miss this enrollment period, except in certain cases where you continue coverage with an employer.

The initial enrollment period is especially important when it comes to prescription drug coverage. Part D plan decisions can only be made at initial enrollment or during the annual enrollment period between October 15 and December 7 each year.

Get help

Medicare.gov offers all the information you need to research the details of your particular situation and explore options with newly redesigned tools to compare plans and pricing.

Independent brokers can also help you analyze your choices. These experts are state-licensed and generally do not charge a fee to consumers.

While individuals understand they can compare at home on their own, they often appreciate working with someone who can help them interpret the results, Kozlowski says. “They find value in having a second set of eyes making sure they’re in the right plan,” he says. “When we work with someone, we help them year after year to make sure they’re always in the best plan for them as an individual.”

Relax

While Medicare healthcare decisions are important, remember they’re not permanent. Plans change every year, and Medicare allows you to make new choices once a year during open enrollment, October 15 through December 7.

If you have Medicare Advantage and want to change your plan, you may make a one-time change during the Medicare Advantage open enrollment period that runs from January 1 through March 31 annually.

Medicare Glossary

Formulary. A plan’s list of covered prescription drugs.

Medicare Part A (hospital insurance). Medicare Part A covers inpatient hospital stays, care in a skilled nursing facility, hospice care and some home health care.

Medicare Part B (medical insurance). Medicare Part B covers certain doctors’ services, outpatient care, medical supplies and preventive services.

Medicare Part C (Medicare Advantage). A private insurance plan that covers inpatient hospital stays, doctors’ services and usually prescription drugs as an alternative to Original Medicare.

Medicare Part D (prescription drug coverage). Medicare Part D adds prescription drug coverage to Original Medicare.

Medicare Supplemental Insurance or Medigap Plans. Additional insurance policies that help pay some of the healthcare costs that Original Medicare does not cover.

Original Medicare. Medicare Part A and Part B are often referred to as Original Medicare.