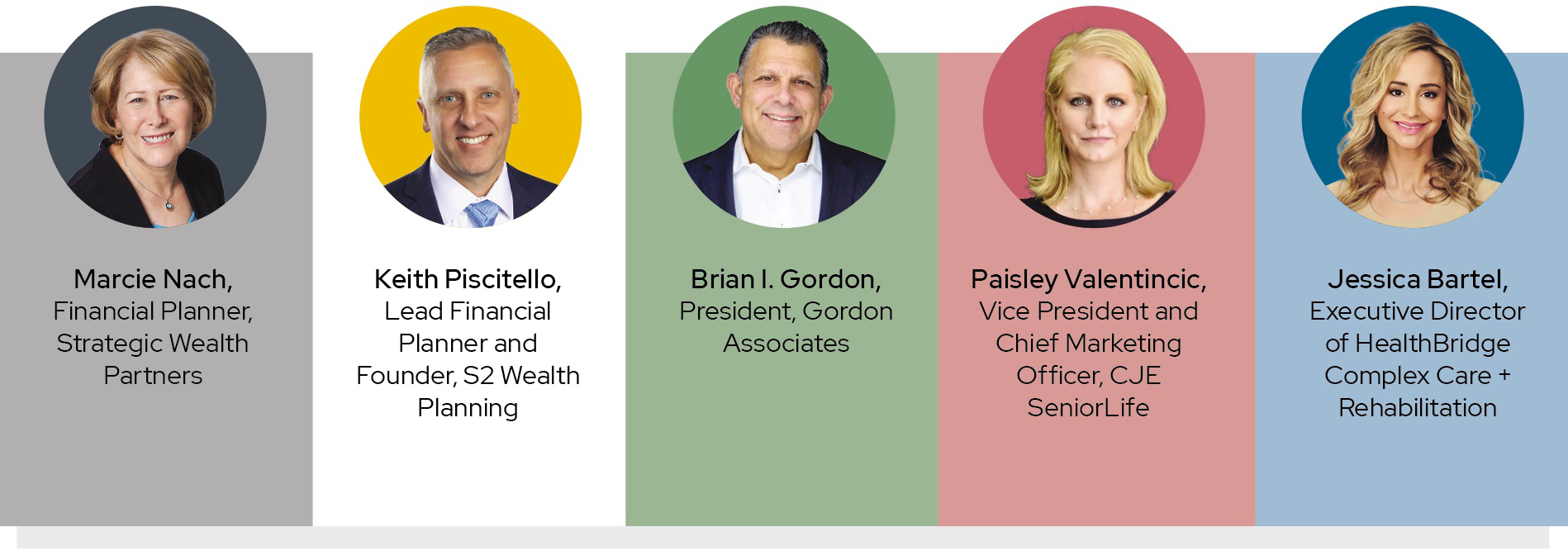

Planning successfully for your future is all about keeping finances foremost in your mind. Everyone needs to stay on top of their money — to know what they’re spending on housing and other budget items, large and small, and how that affects long-term financial health. Here, five financial experts and senior care specialists share their insights on retirement and aging: how to ensure a secure retirement by building strong saving and investing habits early, and how to prepare for funding the ever-increasing costs of aging.

What do you wish more people understood about saving for aging and retirement?

Keith Piscitello: Some scientists believe the first person to live to 150 likely has already been born. Even if the average retirement age increases to 75 years old, that still means that half their life will be spent in retirement. Increases in expected longevity mean an increased importance in proactive planning for funding post-working years.

Keith Piscitello: Some scientists believe the first person to live to 150 likely has already been born. Even if the average retirement age increases to 75 years old, that still means that half their life will be spent in retirement. Increases in expected longevity mean an increased importance in proactive planning for funding post-working years.

Paisley Valentincic: When planning for aging, I hope people recognize the value of starting early and researching all the options. In addition, be flexible and adjust your plan as circumstances change. Implementing a plan is much easier than having to react in a stressful situation. A proactive approach, with well-informed choices, is ideal.

Paisley Valentincic: When planning for aging, I hope people recognize the value of starting early and researching all the options. In addition, be flexible and adjust your plan as circumstances change. Implementing a plan is much easier than having to react in a stressful situation. A proactive approach, with well-informed choices, is ideal.

Brian I. Gordon: If you hope to live a long life, you probably need to save more, and start earlier than you think. Modern medicine keeps us alive longer but not healthier, which means costs of care as one ages are more frequent and go up.

Brian I. Gordon: If you hope to live a long life, you probably need to save more, and start earlier than you think. Modern medicine keeps us alive longer but not healthier, which means costs of care as one ages are more frequent and go up.

Jessica Bartel: That it’s important to take care

Jessica Bartel: That it’s important to take care

of your health. Your health can work for you or against you. If you remain healthy, and free from health ailments, you will save and be better for it in retirement and old age. Look at it this way: Less doctor visits, hospital stays, or even the need for nursing home placement can save dividends in the long run. Take care of your health now, for a healthy tomorrow both physically and financially.

What are some of the biggest challenges in care affordability that your clients face?

Marcie Nach: Not only is the cost of living in an assisted living or long-term care facility prohibitive, but one or both spouses may also need to hire a private caregiver as well. Even if they have long-term care insurance, there is generally a shortfall.

Marcie Nach: Not only is the cost of living in an assisted living or long-term care facility prohibitive, but one or both spouses may also need to hire a private caregiver as well. Even if they have long-term care insurance, there is generally a shortfall.

Brian: Most of our clients are planners, but some unfortunately don’t even have a basic knowledge of the cost of care. This means that often they are not prepared with resources to pay for care when the time comes.

Jessica: They’re not ready for long-term care placement. Mainly this can sneak up on patients with Alzheimer’s disease or dementia that are otherwise physically healthy and need long-term care, especially memory care, at a young age.

Keith: Everybody has a plan for care, whether they believe it or not. Traditional health insurance doesn’t cover long-term care and neither does Medicare. If the risk of paying for care is not transferred to an insurance company through one of the products that can pay for the cost of care, then the default plan is to sell things that you may not want to sell (house, retirement account, investments).

Keith: Everybody has a plan for care, whether they believe it or not. Traditional health insurance doesn’t cover long-term care and neither does Medicare. If the risk of paying for care is not transferred to an insurance company through one of the products that can pay for the cost of care, then the default plan is to sell things that you may not want to sell (house, retirement account, investments).

Which resources do you direct people to?

Paisley: Understanding your personal resources and having a trusted advisor to guide you is crucial. To get started, consider reaching out to a local resource such as your senior center, library, civic government offices, or your physician. These places can provide guidance and referrals. Additionally, in Chicago, organizations like CJE SeniorLife take a holistic and person-centered approach, offering support, referrals, and direct services to seniors and their care partners.

What question do you hear most often from clients about planning for the future?

Keith: How can I know if my money will last as long as I do?

Marcie: The most frequent question is: “When can I retire?” Clients are worried about inflation, healthcare costs, helping family members, and their portfolio lasting for an extended lifetime. They want to be as certain as possible that they won’t run out of money before they commit to taking that step.

Brian: Many clients struggle to discuss their wishes with their loved ones. Even if they have a plan in place or finances set aside, their adult children or family often do not know about their plans and wishes in advance of a health crisis. We also get asked how extended care is paid for when a client does not have long-term care insurance.

Paisley: The question often asked is about timing. While an individual’s journey of aging is unpredictable, seeking assistance and connecting with resources can contribute to enhancing quality of life. Whether it’s accessing medical care, social support, or educational programs, there are many valuable resources available to help individuals navigate the challenges that come with aging.

What are the biggest factors for a secure retirement — owning a home outright, not having debt, long-term planning? Something else?

Jessica: The biggest benefit is securing your funds, in equity versus liability. For example, owning property and having a pension is considered for long-term care placement if needed for healthcare or memory care.

Keith: Beginning investing for retirement as early as possible is a key. Compound growth is like building a snowman, even starting small early will mean more opportunities for the snowball to make rotations. The second-biggest factor is assuming that care will be needed and a plan for funding care has been built. If it’s not needed, you’ll be better off in the end. If it is, you’ll be prepared.

Keith: Beginning investing for retirement as early as possible is a key. Compound growth is like building a snowman, even starting small early will mean more opportunities for the snowball to make rotations. The second-biggest factor is assuming that care will be needed and a plan for funding care has been built. If it’s not needed, you’ll be better off in the end. If it is, you’ll be prepared.

What are some common myths around Social Security that can trip people up in their retirement planning?

Marcie: You can start your retirement benefit at any point from age 62 to 70. Many people think they should claim their benefits as soon as they are eligible. For some people, that may be the right solution, but for many others, waiting until age 70 may be a smarter move.

Keith: One common myth is that the trust fund is going to go broke, so I should start collecting money as soon as I’m eligible just in case there’s no money left.

It’s true that estimates from the Social Security and Medicare Boards of Trustees estimate that 100% of promised benefits will only be available through 2033, at which time the trust fund will only be able to fund an estimated 77% of benefits. Those assumptions are based on the current withholding and payout rates. There are significant changes that Congress can pass to extend full benefits. For an individual who would be entitled to a $2,000 monthly benefit at full retirement age (67), starting receiving benefits at age 62 will result in 30% lower monthly benefits for the remainder of their lifetime. Deferring Social Security benefits until age 70 would increase monthly benefits paid to $2,480. Over a lifetime, the difference could mean an additional $200,000 or more received over 20 years of retirement.

Jessica: That it is a secure payment method, when in reality it does not cover 1/12 of the cost if a skilled nursing stay is needed for you or your loved one.

Is investing in life insurance worth it, or should you add that cash investment to your investment portfolio?

Brian: Life insurance is a tool just like any other tool. There isn’t a yes or no answer since retirement planning is not one-size-fits-all. Whether or not life insurance fits will depend on an individual’s circumstances and overall financial plan.

What’s one financial mistake that you often see people make?

Marcie: Most people do not look carefully enough at their spending and generally underestimate the amount they currently spend or will spend in the future. It is almost a universal truth that people are surprised when they do a deep dive into their actual spending, and it is usually much higher than they expected.

Keith: Another key is not overspending for housing. Keeping fixed monthly costs lower frees up more budget for areas like investing for retirement, insurance, emergency savings, and discretionary spending. Avoid being “house rich and cash poor.”

Jessica: Leaving a hospital against medical advice (AMA). I cannot stress this enough. It will waive the coverage, and leave individuals with an expensive bill.

Brian: Not giving your loved ones a good roadmap when you’re in retirement: where important documents are located, what your wishes are, etc. Your loved ones will be taking care of you. They can only respect your plans if they know what the plans are.

What are some red flags to watch for with financial advisors or wealth managers?

Keith: Many financial advisors focus on investments or annuities. Investments are only a part of a client’s financial situation. Look for a certified financial professional (CFP) who has broad expertise. A CFP can provide guidance and advice on insurance, estate planning, tax planning, Social Security, college funding, gifting strategies and even guidance on positive behaviors for secure financial futures.

Brian: When financial advisors or wealth managers make assumptions on behalf of their client instead of asking. For example, not talking about how costs of care will be paid for and just assuming the client will pay out of retirement funds vs. other sources and exploring alternative options.